December 9, 2018

Financial wellness programs were greeted with great hopes when they first debuted. But is the prognosis for their long-term success starting to flag? Amid signs that such programs have not been as impactful as expected, our latest white paper takes a 360-degree look at three sets of stakeholders—plan sponsors, plan participants and retirement plan advisors—to construct a clearer picture of the state of financial wellness initiatives. Here’s a sneak peek!

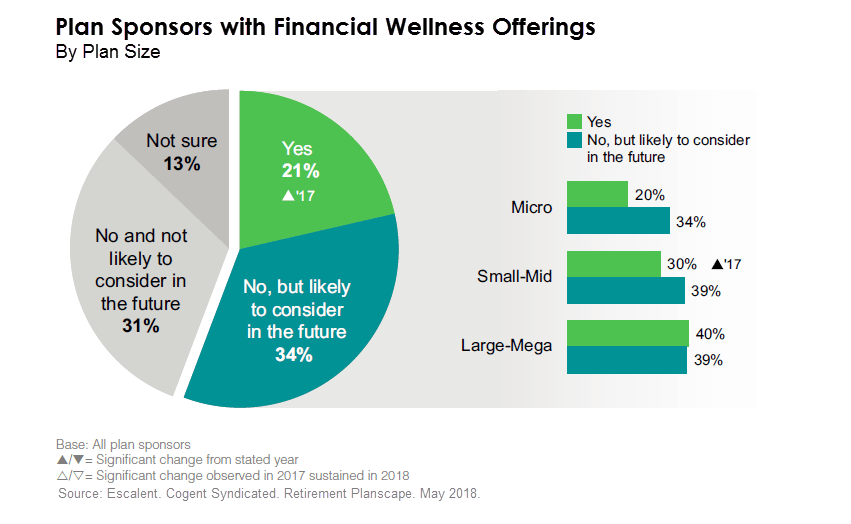

The Employer View: Enthusiastic Adopters

Preparing employees for retirement is a high priority for plan sponsors. Indeed, 40% rank it as one of their top three priorities for the year. It’s no wonder then that employers embrace financial wellness programs with enthusiasm. Adoption rates among plan sponsors jumped from 16% in 2017 to 21% in 2018. And interest in offering a financial wellness program is strong, with over one-third of plan sponsors likely to consider implementing a program in the future.

What Is a Financial Wellness Program?

Cogent Syndicated defines it as a program designed to educate employees about personal financial risks (which may include loss of income due to premature death or illness, unexpected out-of-pocket medical expenses, etc.) and provide tools to manage those risks.

Adoption is highest among Large-Mega plan sponsors, but Micro and Small-Mid employers are increasingly expressing interest. Larger institutions typically have very specific expectations and demand better service from the asset managers they employ. In a phrase, they are harder to please. This year’s Retirement Planscape® report found that among the largest asset holders, just 48% of pensions and 59% of non-profits express satisfaction, yet 76% of smaller pensions and 64% of smaller non-profits are satisfied with their current asset manager relationships.

The unique demands of the largest institutions often drive asset managers to create bespoke strategies to meet the institutions’ specialized needs. This leaves a rich vein of opportunity for innovative firms to target the mid-sized sector with more efficient solutions that offer broader appeal.

Before financial wellness programs die on the vine, providers need to take a closer look at what’s working and what’s not. Poor Prognosis? How to Save a Struggling Financial Wellness Program focuses on the issues for key stakeholders (plan sponsors, plan participants and plan advisors) and offers strategic recommendations for how to improve the prognosis of struggling financial wellness programs.

Interested in learning more about our research on financial wellness? Send us a note and let’s chat!

Linda York

Senior Vice President, Cogent Syndicated

Linda York is a senior vice president in the Cogent Syndicated division where she leads the Wealth Management Syndicated Research & Consulting practice. She has over 20 years of experience in financial services spanning responsibilities in finance, marketing and business strategy. Before joining Escalent, Linda was the practice director of Syndicated Research at Cogent Research, where she managed the product development and execution process for syndicated research projects and consulted with dozens of clients in the retail and institutional wealth management space. She earned an MBA in marketing from the University of Connecticut and a bachelor’s degree in mathematics from Mount Holyoke College. Linda is an avid equestrian and a two-time finisher of the Boston Marathon.