August 20, 2025

The average retirement plan participant aspires to save nearly $1 million in retirement savings across ESRPs, IRAs, taxable brokerage accounts, bank accounts and other investment vehicles. Being able to calculate a retirement savings goal—projecting estimated health expenses, housing costs and discretionary spending among other important variables—is an accomplishment in and of itself, as we’ve reported before. But how do plan participants actually achieve their stated retirement goals? Is it a matter of discipline? Mental fortitude? Good fortune? Or a multitude of factors?

Since 2021, Cogent Syndicated has closely monitored participants’ confidence levels in achieving their stated retirement savings goals, keeping a pulse on shifting sentiments over time. This year, however, we’ve set out to ascertain the key characteristics between those who are highly confident versus those who feel more apprehensive about meeting their ideal savings targets. We also wanted to equip firms with the specific steps they could take to help their participants feel more empowered and to instill in their participants a greater peace of mind.

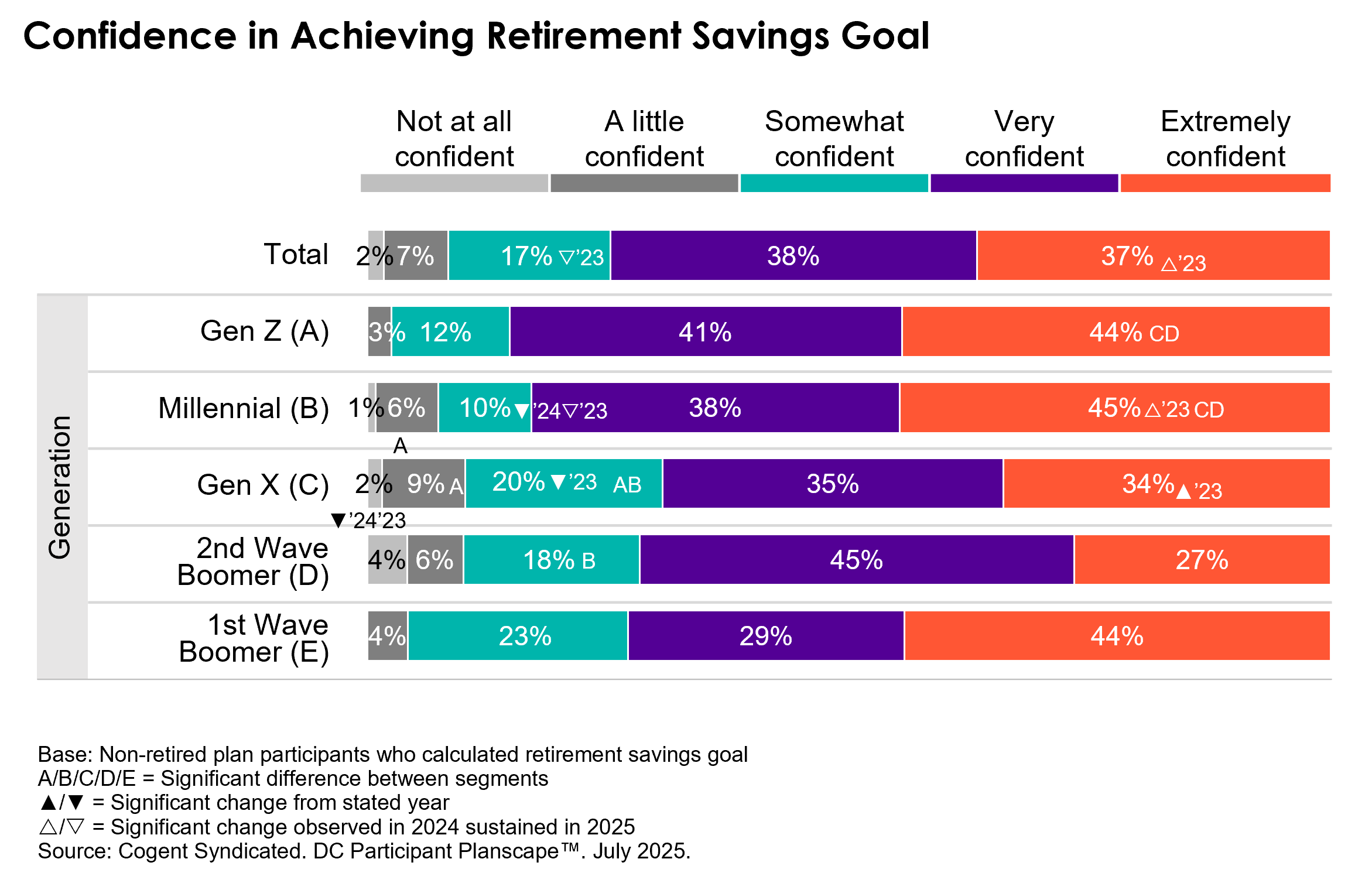

Our latest DC Participant Planscape™ report reveals that more than one-third of plan participants are “extremely confident” in achieving their stated retirement savings goals (37%, a sustained increase from 26% in 2023). In fact, Gen Zers and Millennials are more confident in reaching their retirement savings goals than Gen Xers and 2nd Wave Boomers—even as “extremely confident” ratings are strengthening among Gen Xers (34% vs. 22% in 2023).

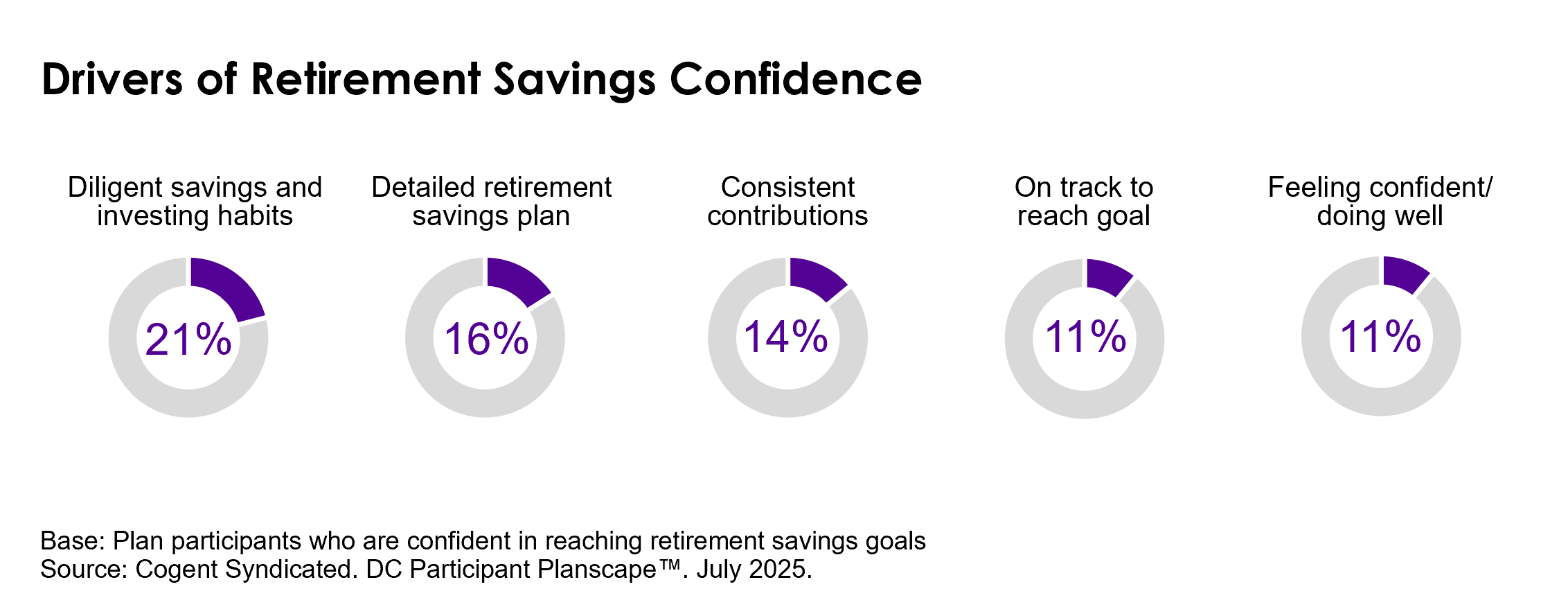

What exactly is driving retirement savings confidence? It turns out participants who are “very” or “extremely” confident are quick to tout the virtues of consistency, automation and a steady mindset. They credit diligent savings habits, detailed retirement savings plans and maintaining consistent, automated contributions regardless of market volatility. Others acknowledge support from their partners and advisors for their success.

“My future husband and I work hard. We are both committed to saving money for retirement.” –Gen Zer

“I have a clear financial plan in place and I contribute consistently …. Having that structure gives me peace of mind and keeps me motivated.” –Millennial

“I automate my savings: 15% of my salary goes directly into my 401(k) with a 5% employer match. I also work with a fiduciary advisor annually to adjust my portfolio, ensuring I stay on track despite market swings.” –Gen Xer

“I have worked out my expenses and consider healthcare costs as well as inflationary issues to meet my goals in retirement.” –2nd Wave Boomer

We also explored the ways providers could better support those who are not as confident in reaching their stated retirement savings goals.

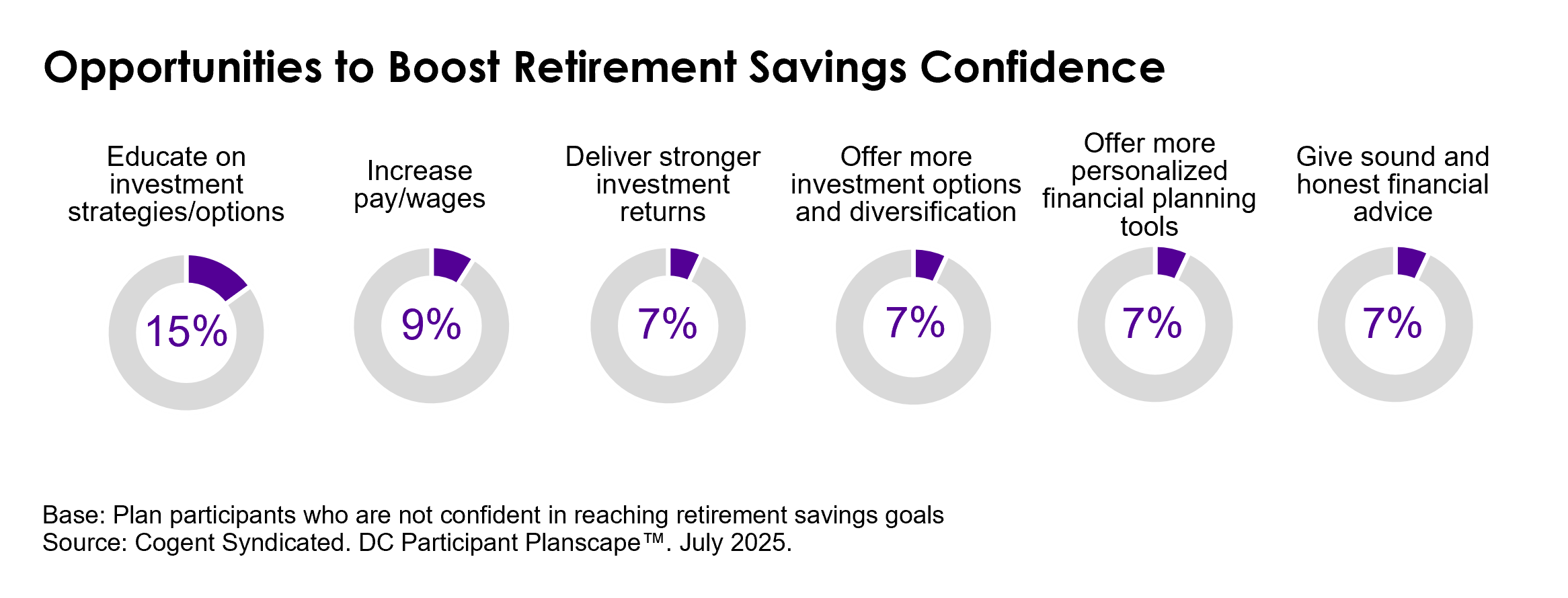

Here, we found participants who are less confident often emphasize education, one-on-one guidance, enhanced tools and even additional perks as ways firms could help boost their respective participants’ confidence levels. Enhanced digital tools and access to customized advice as opportunities are also essential to helping this cohort feel more on track.

“I’d feel more confident if providers gave me tools to see how I’m actually doing, like a simple tracker that shows if I’m on pace for retirement based on my goals … easy-to-understand info or tips, maybe through short videos or emails, so I can make smarter choices without feeling overwhelmed.” –Gen Zer

“Maybe offer some sort of rewards system for regular contribution to the fund or a small percentage added as a sort of ‘cash back’ or commission of sorts for extra funds added.”

–Millennial

“More education and individualized direction. Easier access to sit down and talk to someone.” –Gen Xer

“Just help make a plan to live in my retirement years.” –2nd Wave Boomer

Our full DC Participant Planscape report offers firms a unique understanding of what drives participant contribution and investment behavior. It benchmarks the top plan providers on key satisfaction drivers and brand engagement metrics, monitors the brand perceptions of leading financial services providers and identifies the firms best positioned to capture rollover assets.

For more information on the full report, click below.

Sonia Davis

Senior Product Director, Cogent Syndicated

Sonia is a senior product director in Escalent’s Cogent Syndicated division, where she manages the firm’s defined contribution retirement suite of research with plan sponsors, plan participants and plan advisors. She has more than 15 years of quantitative and qualitative market research experience in financial services industry research, as well as the hospitality, consumer packaged goods and retail sectors. Prior to Escalent, Sonia served as a community manager for C Space, a public relations specialist for Putnam Investments and as a staff reporter for Community Newspaper Company. Sonia earned an MBA from Boston University School of Management and a bachelor’s degree in communications from Simmons University. She’s a proud finisher of the rainiest Boston Marathon on record (2018) and multiple sprint triathlons who now enjoys rowing (sweeps) on the Charles River and outdoor adventures with her husband, two daughters and black lab.