May 21, 2026

Financial advisors are accelerating allocations to alternative investments as private markets, semi-liquid strategies and broader access vehicles become more mainstream in portfolio construction. The latest insights from Cogent Syndicated highlight how adoption patterns, education gaps and evolving product preferences are reshaping wealth management strategies.

The alternative investment landscape is undergoing a dramatic transformation as financial advisors rapidly expand their exposure to private markets, hedge funds and semi-liquid strategies. New findings from Cogent Syndicated’s Trends in Alternative Investments report reveal that advisor adoption and allocation patterns to alternative investments are shifting faster than expected, signaling a fundamental change in how wealth managers approach portfolio construction.

Heavy Users Double Down on Alternative Investments

The proportion of heavy users—advisors allocating 10% or more of client assets to alternative investments—is projected to double over the next two years. Average allocations across all advisors are expected to rise from nearly 8% to about 11%, representing a significant shift in portfolio composition.

This growth is particularly pronounced in the National channel, where the number of heavy users has nearly doubled in just two years, jumping from 14% in 2024 to 27% in 2026. Average allocations to alternatives among National advisors have similarly increased from 5.9% in 2024 to 8.7% in 2026, reflecting deeper conviction and broader adoption across this segment.

What Barriers Are Slowing Alternative Investment Adoption Among Advisors?

Despite this growth trajectory, Cogent Syndicated research shows many advisors remain on the sidelines. Those not using alternatives typically cite client suitability concerns, lack of interest or disappointing past experiences. The key barriers to adoption remain consistent: liquidity constraints, high costs and product complexity. Advisors also report limited knowledge or lack of familiarity as an obstacle, suggesting an education gap that the wealth management industry must address.

Evolving Alternative Investment Product Mix and Positioning

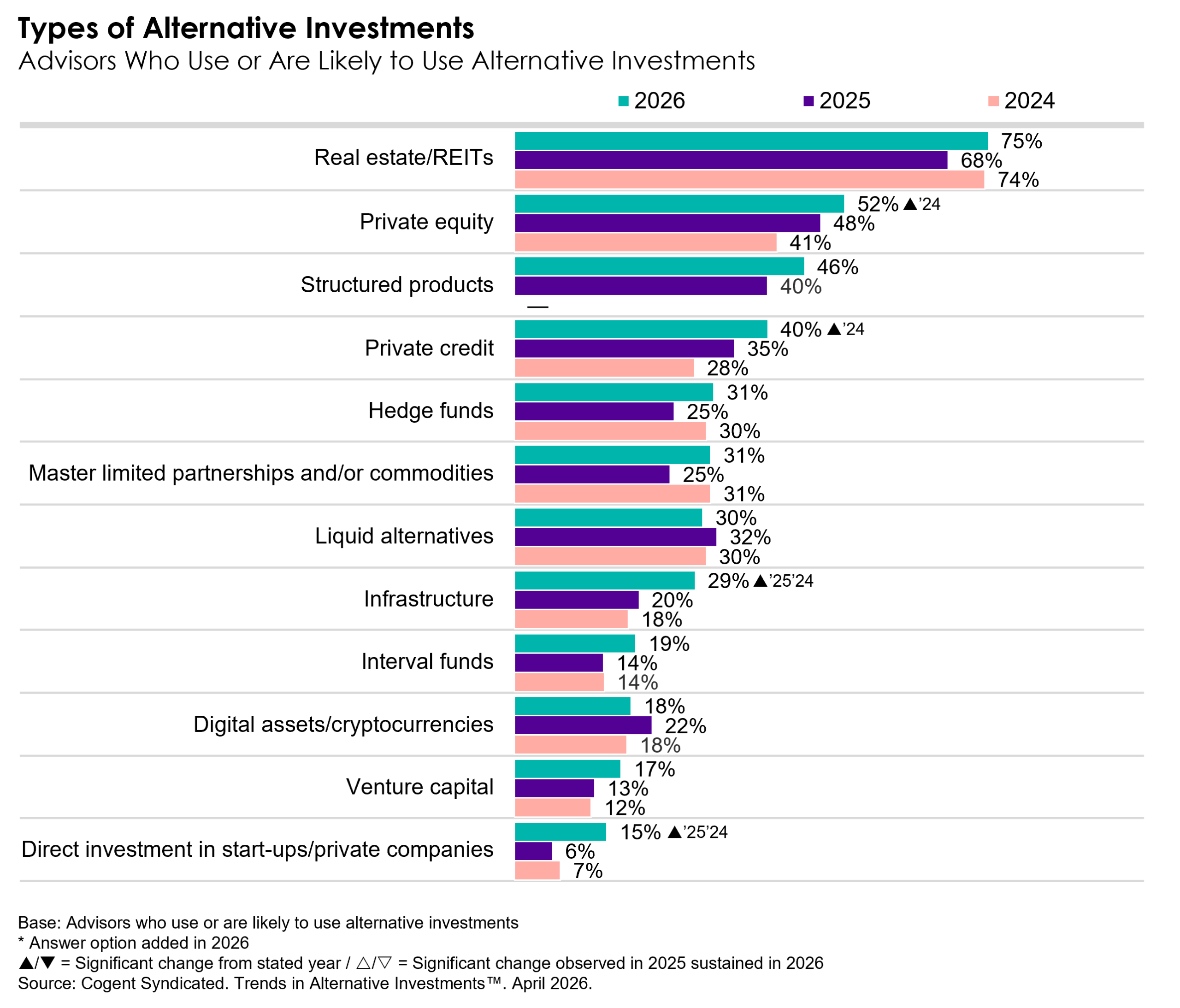

Real estate continues to dominate as the most popular asset class among advisors who are using or are likely to use alternatives, followed by private equity, structured products and private credit. Meanwhile, infrastructure and direct investments have experienced the sharpest year-over-year growth in allocations.

Heavy users of alternatives are driving innovation in product selection, expanding their exposure to private markets, hedge funds, master limited partnerships (MLPs) and infrastructure. These sophisticated advisors are increasingly leaning on closed-end funds and co-investment opportunities to access specialized strategies.

The Alternatives Access Revolution

The distribution landscape for alternatives is changing. While most advisors continue to source products through home offices or internal due diligence teams, direct manager access is rising. Our recent study among financial advisors highlights that this shift is driven primarily by light users as they build out their alternatives capabilities.

Across all advisor types, ETFs and mutual funds remain the dominant investment vehicles, supported by feeder structures that provide individual fund access. This democratization of alternatives through traditional wrapper structures is lowering barriers to entry for advisors who are new to the space.

Why Are Semi-Liquid Alternative Strategies Gaining Traction?

Perhaps the most notable trend is the accelerating adoption of semi-liquid alternative strategies. These vehicles, which offer periodic liquidity windows while providing exposure to private-market returns, are gaining traction among advisors providing to clients who have at least $5 million in assets.

For this affluent client segment, average allocations to semi-liquid vehicles have grown from 14% to 17% among heavy alternatives users, reflecting advisors’ desire to balance access flexibility with the return potential of private markets. This “Goldilocks” approach—not too liquid, not too illiquid—appears to resonate with both advisors and their high-net-worth clients.

Looking Ahead at the Alternative Investment Market

The alternative investment market is at an inflection point. As the proportion of heavy users doubles and average allocations climb toward double digits, alternatives are moving from niche strategies to mainstream portfolio components.

The challenge for wealth firms is addressing knowledge gaps, streamlining access and developing products that meet advisor demands for flexibility, transparency and reasonable fees.

As alternative investments move into a more central role among advisors and investors, our Trends in Alternative Investments study from Cogent Syndicated provides insights into current alternatives use among advisors and investors, sentiment and decision drivers to help asset managers inform product development, distribution strategy and messaging. To learn more about the full report, click below.

Kristin Hall

Product Director, Cogent Syndicated

Kristin recently joined Cogent Syndicated as a Product Manager for Advisor and Investor Insights On Demand products. She has over ten years of experience in the investment industry spanning roles from investment analysis, retirement planning and marketing research. Before joining Cogent Syndicated, Kristin was an Insights Analyst managing a variety of quantitative research projects for Escalent’s primary research clients. Kristin holds an MBA in International Business from Thunderbird School of Global Management and a bachelor’s degree from California Lutheran University. She is also a cellist and performs with a local symphony in Southern California.