April 7, 2025

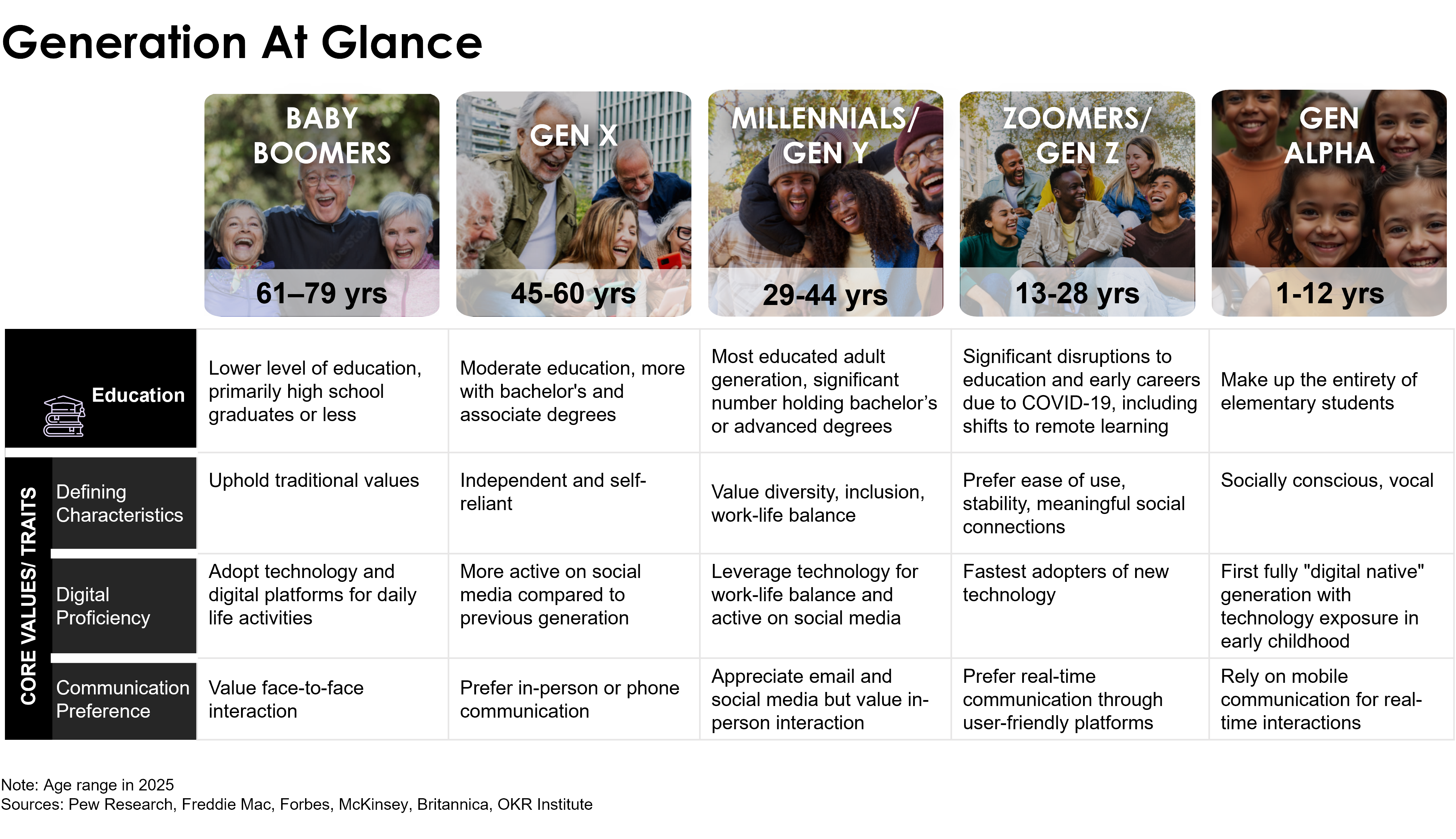

Life Triggers, Generational Differences and Life Experiences

It’s a familiar saying that life insurance isn’t bought—it’s sold—and the insurance industry has long relied on life event triggers such as college graduation, marriage, homeownership or a new baby to guide their sales targeting strategies. For decades, when these major life events occurred, insurance marketers traditionally turned to the old standby—direct mail—to try and engage new parents or homeowners.

And while many insurance companies have incorporated digital communication to try and keep up with changing consumer preferences, insurers’ underlying messaging strategy has largely remained unchanged. However, treating everyone who’s in a similar life stage the same way ignores critical generational differences in attitudes and communication preferences.

For example, a Gen Z first-time parent who is a digital native and trusts influencers more than insurance agents will approach their child’s arrival very differently than their boomer/Gen X parents did. Consider these stats:

- Gen Xers are the most likely age cohort to consult an insurance agent (47%).

- Gen Zers seek guidance from friends and family at a higher rate than any other age group.

- More than 50% of Gen Zers and millennials versus just one-third of boomers consider instant quotes very important.

(Source: Escalent Secondary Research)

While major life events are still important indicators of insurance needs, capturing prospects’ attention requires an understanding of how different generations approach these milestones. Escalent recently conducted secondary research into life stages and generations to uncover the differences in consumer communication styles, preferences and buying habits. With these insights and strategic recommendations, you’ll have the tools you need to ensure your messaging is on time and on target, no matter which segment you’re trying to reach.

Where Traditional Life Insurance Marketing Plans Fall Short

Unlike car or home insurance, life insurance isn’t obligatory, which means firms must time their outreach efforts to coincide with when prospective buyers are most receptive. This is why life insurance marketing has been traditionally tailored to life stages around demographic criteria.

However, sending the same, generic message to all newlyweds isn’t going to deliver optimal results. Layering on generation and life experiences can help you develop a messaging strategy that will more likely be seen by and resonate with target customers. This could include things such as which sources of information they trust most, along with communication preferences and purchasing behaviors.

Generational differences can also profoundly affect how people approach life insurance. For example, many millennials entered the workforce with significant student debt, who for some, led to delays in milestones such as homeownership or starting a family. This created a ripple effect on insurance needs and purchasing behavior.

By targeting individuals with the right message at the right time via the channel they’re most likely to consume and engage with, your brand will stay front and center at purchase time.

A Deeper Dive Into the Layered Approach for Insurance Marketing

When we further analyzed the data, we uncovered foundational differences in the way different generations communicate and source information.

Most trusted information sources: While 46% of baby boomers seek advice from an insurance agent, only 29% of Gen Zers choose agents as their primary information source, more often turning to friends, family and online influencers instead.

Communication preferences: Many traditional life insurance companies continue to invest heavily in direct mail marketing campaigns, constantly refining their list strategies as response rates decline year-over-year. However, this approach ignores the preferences of younger, digitally inclined consumers who rarely check their physical mailboxes and when they do, are far less likely to open what they view as “junk mail.”

- 74% of Gen Zers and millennials state online reviews significantly influence their purchasing decisions. Boomers are the least influenced, at 54%.

- Millennials and Gen Zers are twice as likely to depend on video reviews compared with boomers.

As boomers reach retirement—typically around age 65—companies relying solely on traditional “snail mail” will face a shrinking audience. In addition, continuing to use less relevant marketing methods could negatively affect brand perception, signaling to younger consumers the company is behind the times.

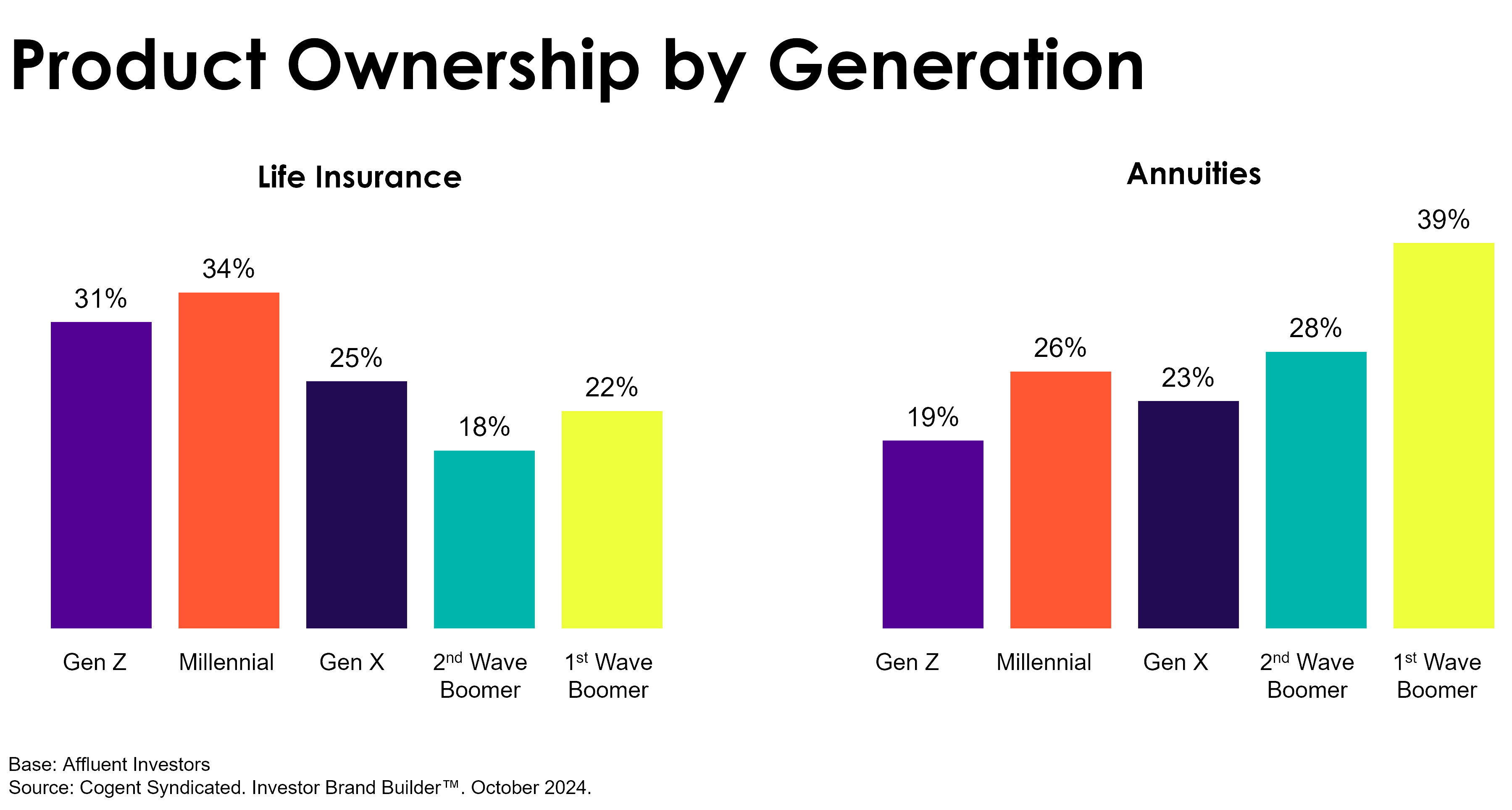

Propensity to buy: The 2024 Cogent Syndicated Investor Brand Builder study has found that younger generations have higher interest in and propensity to own life insurance. According to the study, 34% of millennials with at least $100,000 in investable assets own a life insurance product, higher than all other age cohorts. In addition, 26% report owning an annuity, compared with only 23% of Gen Xers.

While this is good news for insurance companies, it’s important to balance propensity to buy with trusted information sources and preferred purchasing methods. As mentioned above, younger consumers are less interested in having insurance sold to them by commissioned agents, preferring more transparent, direct-to-consumer purchasing options instead.

Three Steps to Ensure Life Insurance Marketing Breaks Through

Stop treating everyone in similar life stages the same way: People starting second families later in life won’t respond to a value proposition written for new, young parents. In addition to rethinking how and what you communicate with these customers, you might consider recasting the life insurance product itself to fit their specific needs. This starts with listening to and understanding what kind of messaging speaks directly to your target audience.

John Hancock is a great example of a company that listens to its customers and fills a need. Hancock’s Vitality program rewards customers for making healthy choices such as eating the right foods, walking the dog or keeping up with preventive checkups. Customers can earn fitness wearables and gift cards or get a discount on their premiums for participating.

Be aware of preconceived notions about insurance: Buying a first car is an emotional experience for many consumers. The shiny paint, the new car smell-it’s all exciting. Buying a life insurance policy isn’t as thrilling. If consumers already have it in their mind that the purchase will be uneventful, they’re more likely to simply shop around for the best price to get it over with.

Preconceived notions also impact propensity to buy. Our finding that millennials score very high on propensity to buy could stem in part from their fears that Social Security won’t be around to take care of them when they retire. However, these younger consumers are less likely to complete a purchase if they have to deal with an agent, so marketers should do their homework around purchasing preferences.

Shake up your communication mix: If you want to attract the next generation, or the generation that follows, it’s important to consider different approaches. In addition to using more digital channels such as social media and influencers for younger consumers, borrow ideas from other industries and scenarios when developing insurance marketing campaigns.

For example, with the help of C Space’s generational research, McDonald’s was able to create stronger connections with the 18- to 24-year-olds to drive cultural relevance to that segment of their target market. Through an 18-episode professionally created video series, McDonald’s employees were able to better understand that consumer segment’s choices, behaviors and personalities to make the company more relevant to a key consumer target.

Insurers today are making significant investments in data analytics and targeting growth during this period of higher interest rates. To find out more about how Escalent can help you move away from an overreliance on traditional media and messaging, and in doing so, better connect with younger audiences through a deeper understanding of generational differences, drop us a note today.

Want to learn more? Let’s connect.

Jeremy Bowler

Senior Vice President, Financial Services

Jeremy Bowler is a senior vice president in the Financial Services Research division of Escalent, with more than 25 years of experience in marketing and market research, the majority being in the financial services and insurance sectors internationally. He manages strategic business development in proprietary Voice of the Customer research and consulting services. Prior to joining Market Strategies, Jeremy spent 14 years at J.D. Power and Associates. While there he developed industry benchmarks in the insurance, healthcare, banking and mortgage industries, and led the Global Insurance Practice, providing syndicated and proprietary research as well as consulting solutions. A frequent presenter at industry events, Jeremy has authored or contributed to numerous trade publications, including BusinessWeek and A.M. Best’s Best Review. Jeremy earned a bachelor’s degree in physics and economics from the University of Michigan.