October 14, 2020

Changes that were already under way in the advisory business are accelerating amid the backdrop of the COVID-19 pandemic. At the same time, the makeup of the advisor population is changing as more advisors approach retirement and firms work to attract younger advisors. With all of these factors in play, financial services firms need to focus on meeting the needs of the next generation of financial advisors. Through adjusting outreach strategies and optimizing service models to meet younger advisors’ expectations, firms have an opportunity to ensure ongoing relevancy for years to come.

Due to COVID-19, advisors report increasing their reliance on digital and remote tools (e.g., phone calls, video conferencing, emails) and decreasing their use of traditional tools (e.g., sponsored events, in-person meetings) to communicate with clients. These changes in communication means are giving advisors the freedom to consider longer-term shifts in their business structure. For example, advisors are increasingly assuming the mindset that working from home at least part of the time will be the new normal. Three in ten advisors plan to have fewer in-person interactions with clients even after the pandemic is over.

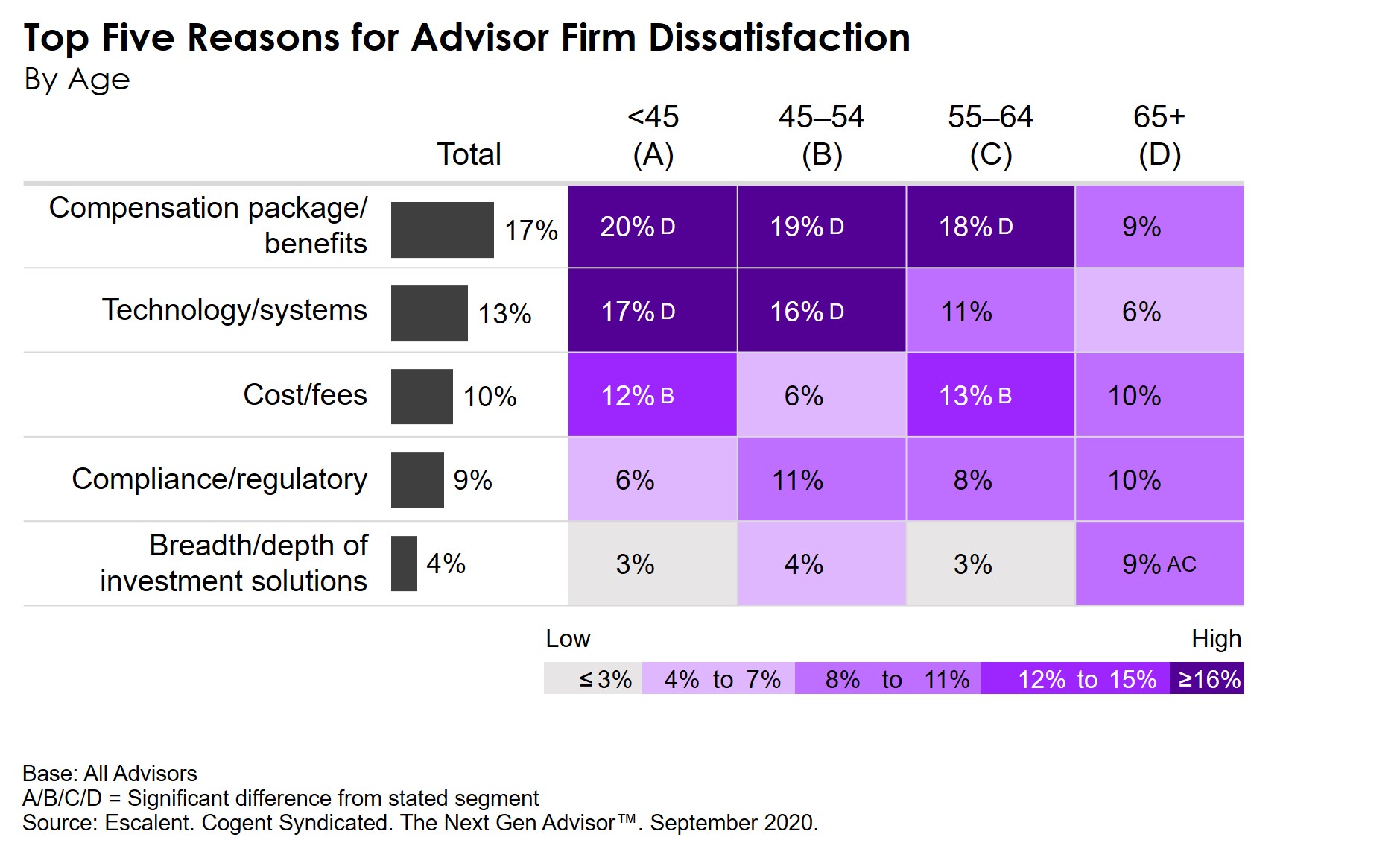

This shift toward remote work and digital communication has implications for how advisors engage with their employers as well as asset managers. Overall, 13% of advisors cite technology systems as a source of dissatisfaction with their current firm, with younger generations expressing even greater dissatisfaction with tech. Advisors younger than 45 are more likely than their older peers to have recently turned to new technology tools, especially video conferencing, to help manage their business. When engaging with asset managers, wholesaler interactions are also now taking place remotely through the phone and video conference. This temporary need gives providers an opportunity to gauge the effectiveness of these types of virtual interactions and increased accessibility in the longer-term, particularly for younger advisors who are interested in more-frequent wholesaler interactions.

With the current advisor population aging, there is a growing urgency for transition planning and developing a better understanding of the unique challenges in meeting younger advisors’ needs. A few generational differences we uncovered:

- Advisors younger than 45 are almost twice as likely to work in teams compared with their older peers.

- The youngest advisors (younger than 45 years old) will be primarily responsible for driving increased use of model portfolios and have less conviction in the value of active management.

- Younger advisors work with the fewest mutual fund providers and tend to report weaker loyalty to the firms they are using.

- There are some notable differences in drivers of consideration and brand perceptions among younger advisors.

The Next Gen Advisor™, our newest Cogent Syndicated report, uncovers these and many other generational differences in needs and preferences of financial advisors. Click below or send us a note to learn more about the full report.

Meredith Lloyd Rice

Vice President, Cogent Syndicated

Meredith Lloyd Rice is a vice president in Escalent's Cogent Syndicated division. She manages the firm’s syndicated research products focused on the financial advisor market and is the lead author of the Advisor Brandscape® report. She has more than 15 years of experience managing research initiatives in the wealth management industry and has explored a wide range of business issues on the client and supplier side. Prior to joining Escalent, Meredith was an associate VP at Chatham Partners where she oversaw a team of researchers and managed the overall design, analysis and interpretation of large-scale studies for institutional financial services clients. Meredith earned an MBA from Thunderbird School of Global Management and a bachelor’s degree from Colgate University. She is a former collegiate rower who now gets her exercise chasing after her daughter and Clumber Spaniel.