December 5, 2024

Retirement Plan Advisor Trends™ report from Escalent reveals increasing demand for retirement income solutions, but no clear “solution” exists

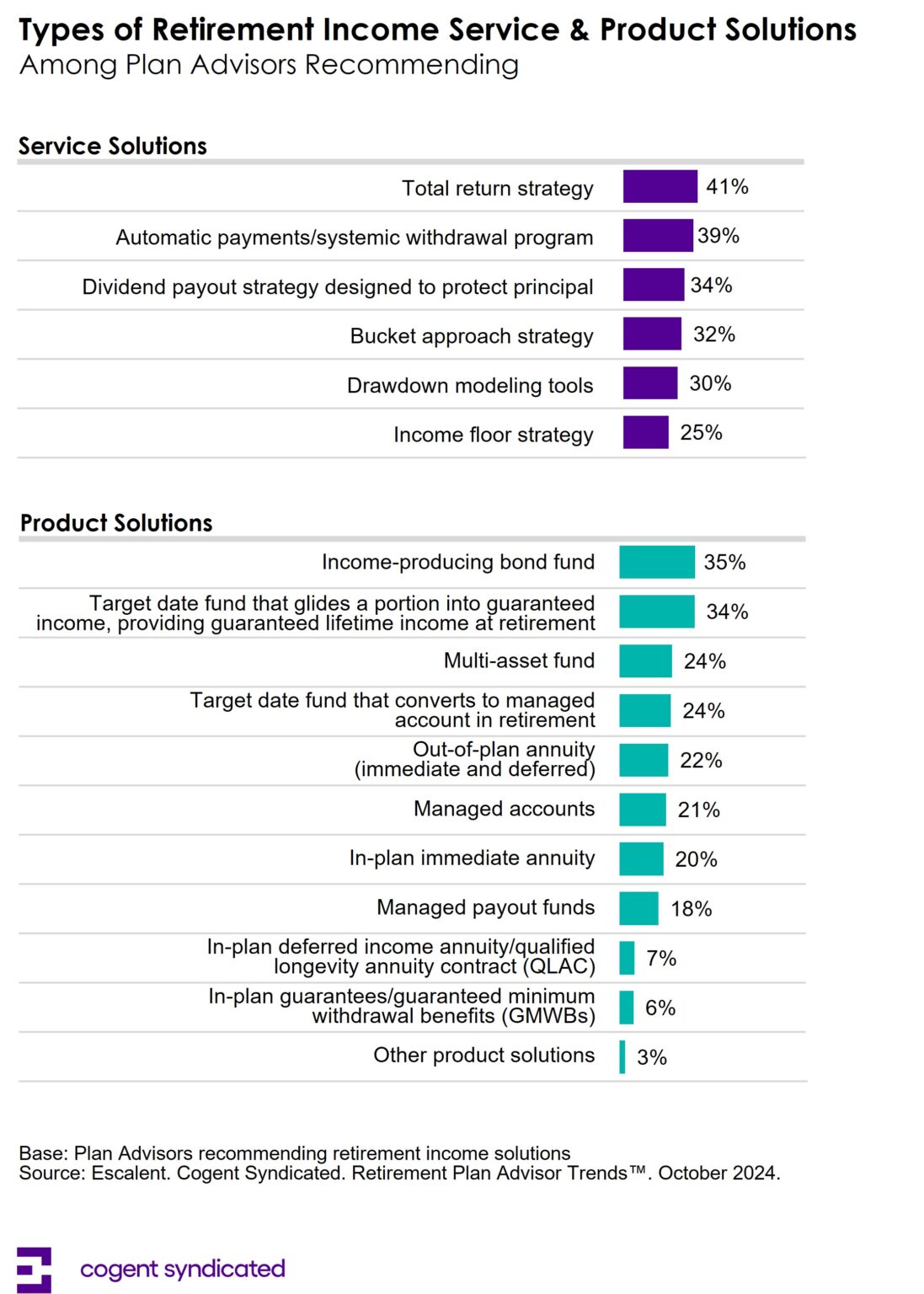

Retirement plan advisors are increasingly advocating for retirement income solutions to help plan participants navigate the draw-down years, yet the “solution” remains amorphous, as multiple services and products are being vetted. Three in ten defined contribution (DC) advisors are actively recommending retirement income solutions (30%, a significant increase from 21% in 2022), with another 40% saying they are likely to do so in the future. Despite this growing demand, no single service or product has emerged as the clear front-runner, suggesting continued industry innovation is needed.

These are the latest findings from Retirement Plan Advisor Trends™, a Cogent Syndicated report from Escalent that examines the attitudes, behaviors and preferences of financial advisors who sell and support DC retirement plans. This annual study explores emerging trends and the role of advisors across all channels, benchmarking leading DC plan providers and DC investment managers on brand equity and experience.

“As more Baby Boomers reach retirement age and many Gen Xers find themselves caring for elderly parents, plan participants are rightfully nervous about the potential of outliving their savings. Contributing to employer-sponsored retirement plans is designed to be easy, but help is needed traversing the decumulation phase — understanding how to withdraw, convert and maximize their savings for decades to come,” said Sonia Davis, lead report author and senior product director at Escalent’s Cogent Syndicated division. “As such, DC advisors are evaluating the success of retirement income solutions based on participant feedback, asset preservation and longevity planning.”

The Cogent study found multiple product and service solutions in play. For example, one-third of DC advisors are recommending income-producing bond funds and target date funds that glide a portion into guaranteed income. Meanwhile, four-in-ten DC advisors are turning toward total return strategies or automatic payments/systematic withdrawal programs.

The report also reveals that concerns over high fees and expenses are the biggest hurdle to adoption, especially among producers managing $50 million or more in DC assets. Other top obstacles include portability concerns and perceived lack of demand from participants, a clear disconnect when compared to recent data from Escalent’s DC Participant Planscape™ study.

“According to our latest plan participant research, only 17% of plan participants feel extremely confident in their ability to convert retirement savings into real-life income, with Gen Xers citing the most apprehension,” said Davis. “For providers, this highlights the opportunity for more DC advisor education and underscores the vast revenue potential of retirement income solutions for those firms willing and able to innovate.”

About Retirement Plan Advisor Trends™

Cogent Syndicated, a division of Escalent, conducted an online survey of a representative cross-section of 411 plan advisors from September 9 to September 17, 2024. Survey participants were required to have an active book of business of at least $5 million and be actively managing DC plans. Strict quotas were set during the data collection period, and post-fielding statistical weighting (where necessary) was applied. The data have a margin of error of ±4.83% at the 95% confidence level. Escalent will supply the exact wording of any survey question upon request.